Index insurance in Vietnam: a new case for blockchain?

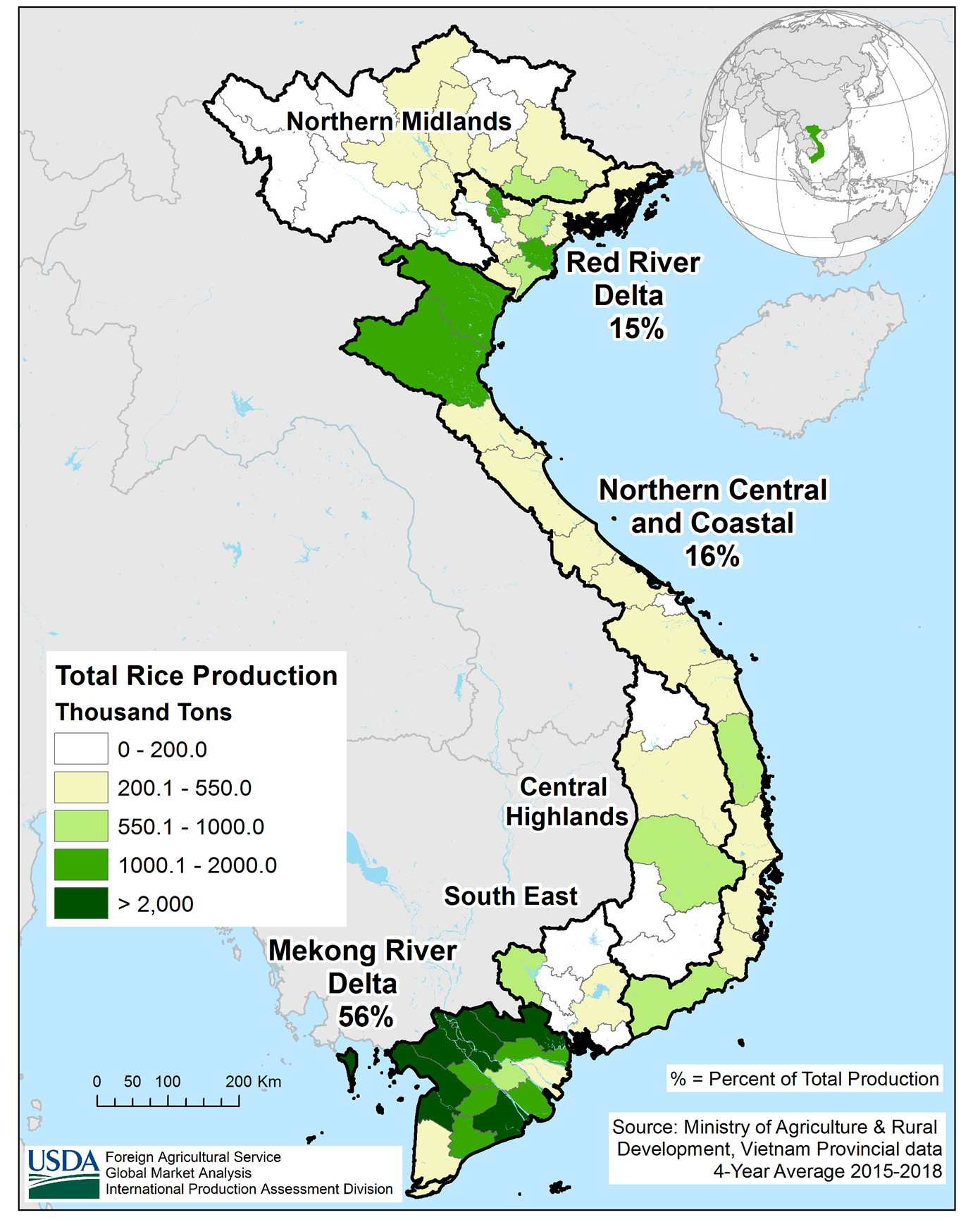

Rice production in Vietnam is a serious business, though not without looming challenges. Worldwide, the country is the fifth-largest consumer and the third-largest exporter of rice. Around 95% of the rice Vietnam exports is produced in the Mekong Delta – the country’s most productive agricultural region (Figure 1). The Delta’s wet and low-lying coastal geography has made it a fertile breadbasket for many years. However, rice production is hampered each year by the impact of climate change. Floods, varying rainfall patterns, saltwater intrusion and coastal erosion have affected paddy farmers’ yields.

Figure 1: Rice production by region in Vietnam, 2015 - 2018

Source: USDA Foreign Agricultural Service

Such weather-related shocks can lead to income volatility for the millions of smallholder farmers that produce rice and other cereal. In turn, lower incomes can trap farmers and households in a twin poverty-and-debt trap. Risk exposure in this manner could dampen farmers’ enthusiasm to pursue farming practices designed to mitigate the risks they face. Why should a farmer adapt their way of producing rice if there is no guarantee of a stable income? This is where agricultural index insurance can be introduced to improve farmers’ resilience to the impact of climate change and protect their livelihoods.

In November 2022, Igloo – a Singapore-based InsurTech – launched Vietnam’s first weather index insurance product: a blockchain-based solution that automates claims through smart contracts. The scheme relies on a public-private partnership, involving local insurer PVI Insurance, the Vietnam Meteorological and Hydrological Administration (VNMHA) and global reinsurer SCOR. The product was designed by Weather Risk Management Services (WRMS), a technical service provider and a new institutional member of the MiN.

The product was launched to protect rice smallholder farmers in the Mekong Delta against insufficient and excessive rainfall. Paddy in this region is typically sown across three seasons: January to May (winter-spring), March to September (summer-autumn, early), and July to December (summer-autumn, late). The pilot season (January to May) is expected to cover 5,000 hectares, rising to 50,000 hectares for the next three seasons. Farmers may purchase cover for a minimum area of 0.1 hectares, with no maximum area.

Key details on Vietnam’s first index insurance product for the pilot season

| Premium per farmer per hectare | USD 8 |

| Minimum landholding covered | 0.1 hectares |

| Total sum insured per hectare | USD 170 |

| Maximum pay-out for insufficient rainfall | USD 42.5 |

| Maximum pay-out for excessive rainfall | USD 127.5 |

| Total area covered | 5,000 – 6,000 hectares |

| Provinces covered | Eight provinces (An Giang, Ben Tre, Ca Mau, Can Tho, Dong Thap, Hau Giang, Kien Giang and Long An) |

| Season | Winter-spring (January to May) |

Developing the product was not straightforward. While the VNMHA provided ground-level rainfall data for the insurable areas, data gaps could have affected the product’s design and pricing – particularly as it is bundled with loans. To avoid this, WRMS adjusted the product to minimise basis risk and ensure a strong correlation between actual yield shortfall and pay-outs in worst-loss years. This approach also accounted for data outliers. Beyond product design, WRMS will play an important role as the calculating agent.

WRMS has pioneered the development and implementation of parametric insurance products for Fiji, Haiti, India, Tonga, Cambodia, Vietnam, and Bangladesh. Our full-stack digital-first risk management platform provides a comprehensive solution to the end-user. This includes product development and validation, data management, user onboarding, product education, claims calculation, and pay-out. Our aim is to build the resilience of vulnerable communities by improving access to sustainable, efficient, and affordable risk management solutions for better disaster response and recovery. Neha Batra, Head – Risk & Underwriting, WRMS |

WRMS has launched the first-ever index insurance products for several countries. In Fiji and Haiti, WRMS developed a product for the United Nations Capital Development Fund (UNCDF) and the World Food Programme (WFP) respectively. SCOR’s prior experience with WRMS in Haiti led to the latter’s involvement in Vietnam. Technical service providers often bring reinsurers on board to index insurance schemes. This case was different: SCOR recommended that WRMS design this product for Vietnam – given their prior experience working together.

The operating model sets this scheme apart: it relies on a combination of typical index insurance technology and blockchain. Pay-outs will be made to farmers automatically when rainfall indices are triggered using real-time data from the VNMHA. Uniquely, this product relies on a public blockchain to host the business rules on how claims are paid out. Using blockchain can make the pay-out process transparent and consistent, and offer credibility from the onset.