Blue Marble Microinsurance and Nespresso: Lessons from a model crop insurance scheme

In June 2024, the Microinsurance Network hosted its annual event for its members in Luxembourg. Known as the June Member Meeting, around 50 individuals from all over the world spent three days discussing the challenges that the microinsurance sector faces, and opportunities for future growth. The event’s centrepiece is the ability to learn about how different organisations are progressing in their respective regions, and what might be driving their success.

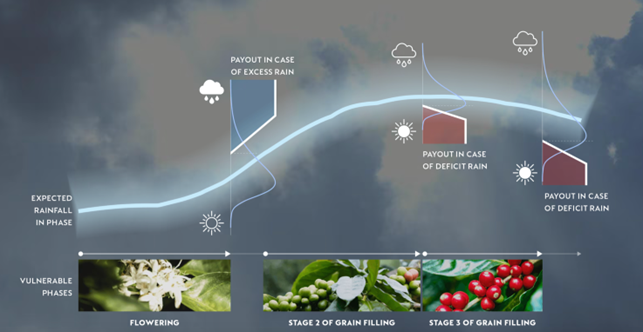

Several organisations showcased how they had been impacting customers in their target regions, including Blue Marble Micronsurance in Latin America. Blue Marble has been making subtle waves in the inclusive insurance space for several years. In 2018, the insurtech partnered with Nespresso to insure smallholder coffee farmers in Colombia. Initially launched as a pilot, known as Café Seguro, the scheme was designed to protect farmers against the main climate risks they typically face: excessive rain during the coffee tree’s flowering phase and a lack of rain during the grain-filling phase (Figure 1).

Figure 1: Café Seguro’s payouts, based on a coffee tree’s phenological phases

Source: Nespresso

Providing crop insurance offers one way for private enterprises to demonstrate sustainability as a company value. For Nespresso, the objective was to improve farmer resilience as part of its “Positive Cup” strategy, which reinforces the idea that coffee should be a force for good. The strategy is designed to empower farmers and enable them to improve their livelihoods, prosperity and resilience through high-quality coffee production. Crop insurance also offers an opportunity to strengthen supply chain resilience.

The partnership between Blue Marble and Nespresso began in Colombia in 2018. As of 2020, Colombia was the fourth-largest coffee producer worldwide. Coffee production is the main source of income for more than 500,000 families that rely on agriculture and accounts for around 700,000 jobs in the country. The programme has since scaled to cover smallholder coffee farmers in Guatemala, Honduras, Indonesia, Kenya and Zimbabwe.

Why Colombia is an ideal location to pilot crop insurance for coffee farmers

The assumed impact of climate change to coffee production in Colombia is likely to affect some farmers in the future. Climate data collected between 2007 and 2013 in the country’s 521 coffee-producing municipalities was modelled to determine future production from 2042 to 2061 as part of an academic study. The results found that while productivity is expected to rise at a national level, farmers in low altitude regions (below 1,500 metres) may see an eight percent drop in production. Rising temperatures may benefit areas that are currently marginal for coffee-growing, while areas that are currently prime coffee-growing locations may be too hot and dry in the future.

“Adverse weather in Colombia in 2022 led to a challenging year for coffee growers. Our original programme, Café Seguro, paid out around $3m to 6,475 smallholder coffee farmers in the country.” Jaime de Pinies, CEO – Blue Marble Microinsurance |

In this scenario, the challenge for Blue Marble was to design a bespoke, affordable crop insurance scheme that can pay out quickly – without delay – when adverse weather impacts coffee production. The target farmers had no proper access to affordable climate insurance. The scheme was launched in partnership with Cafexport, a coffee buyer, and Seguros Bolivar, an underwriter.

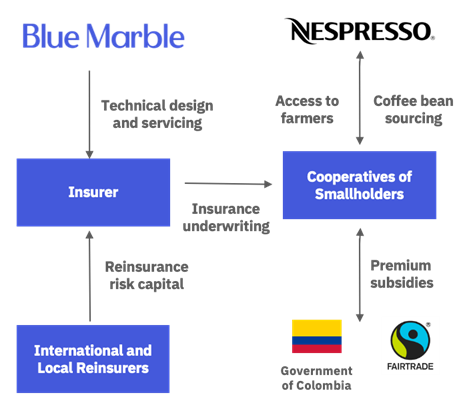

The scheme has since evolved to include several smallholder co-operatives, traders and the Fairtrade Foundation. Insurance premiums were initially paid by the co-operatives. Currently, premiums are covered by a combination of subsidies from the Government of Colombia, the co-operatives’ Fairtrade premiums and farmers themselves (Figure 2).

Figure 2: How Blue Marble and Nespresso’s partnership breaks down

Source: Blue Marble Microinsurance

Like most parametric insurance solutions, the scheme relies on satellite data to determine when coffee production has been affected by either excess or insufficient rainfall. When the parametric index is triggered, payouts are made directly to the registered coffee grower of the affected area, based on the severity of the weather they are assumed to have experienced. From the programme’s start through 2023, the scheme has paid out just under $7m in cumulative claims to approximately 190,000 beneficiaries.

A model for public-private partnerships?

Beyond the statistics, there are a few laudable attributes about this particular example of parametric insurance. The first is its longevity: it is well-known that many crop microinsurance schemes have stopped abruptly, especially after encouraging starts, often due to a lack of premium funding. Blue Marble and Nespresso’s partnership shows a graduated approach to encouraging the beneficiary to ultimately start paying for their insurance cover. The Government of Colombia – through subsidies – has also played an important role in ensuring the scheme’s sustainability.

The second is how the scheme distinguishes itself from other parametric insurance solutions. Often, the focus on new products can be about the extent to which emerging technology is applied in a clever way. However, in this case, a key feature is the use of larger payouts based on weather inclemency – rather than an all or nothing payout that is synonymous with index insurance. This has likely led to a healthy degree of trust in insurance among the target farmers.

Finally, Nespresso’s commitment to the scheme across several countries exemplifies the attributes needed for an effective private-sector partnership. Having national government support is key too, with the Government of Colombia recognising coffee’s economic importance. This is where other index insurance providers have struggled: getting agriculture-dependent governments to appreciate how crop insurance can protect their ongoing investments and future income. Perhaps this example can serve as a replicable blueprint on how to develop crop insurance that can work for all value-chain participants.